Manufacturers Welcome Interior’s Offshore Leasing Plan to Unleash American Energy Dominance

Washington, D.C. – Following the Department of the Interior’s announcement today of a new offshore leasing program, National Association of Manufacturers Managing Vice President of Policy Charles Crain released the following statement:

“Manufacturers welcome the Department of the Interior’s plan to expand offshore oil and gas development. Secretary of the Interior Doug Burgum is taking a critical step to unleash American energy dominance and drive down energy prices. Today’s action also underscores the need to advance streamlined, durable permitting reform that ensures new energy projects can move forward quickly while protecting the environment.”

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

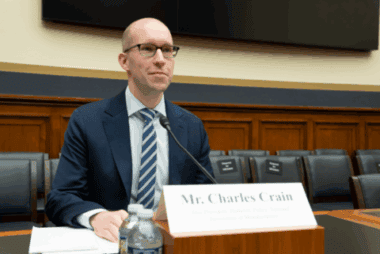

ICYMI: NAM’s Charles Crain Testifies Before House Small Business Committee

Washington, D.C. – Today, National Association of Manufacturers Managing Vice President of Policy Charles Crain testified before the House Small Business Committee at its hearing, “Made in the USA: How Main Street Is Revitalizing Domestic Manufacturing.”

In his testimony, Crain thanked the Small Business Committee for its leadership on the recent tax reform package, which made pro-growth, pro-manufacturing tax policy a permanent part of the tax code, giving small and medium-sized manufacturers much-needed certainty. However, by addressing other ongoing challenges, Congress can strengthen and protect the success of H.R. 1.

In his opening remarks, Crain outlined the opportunities:

“Congress and the administration can pursue what we’ve called a ‘comprehensive manufacturing strategy.’

- That means rebalancing unworkable regulations and reforming America’s broken permitting process;

- It means investing in our nation’s infrastructure and supporting American energy dominance;

- It means providing trade certainty that empowers manufacturers to make things in America;

- And it means investing in the manufacturing workforce of the future.

“We need all of these policies to build on the success of tax reform, to unlock small manufacturing growth and to drive a true manufacturing renaissance.”

He closed his remarks by encouraging the committee to build on this year’s success:

“This is the road to a manufacturing renaissance. It runs through a comprehensive manufacturing strategy—ensuring that all parts of the federal government are rowing in the same direction: toward an empowered, emboldened, exceptional manufacturing industry.

“Backed by the right policy choices, small manufacturers will deliver—for our communities, for our country and for our preeminence on the world stage.

“Because when manufacturing wins, America wins.”

Read Crain’s full written testimony here.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Timmons: EPA’s Revised WOTUS Rule Brings Certainty and Predictability for Manufacturers

Washington, D.C. – Following Environmental Protection Agency Administrator Lee Zeldin’s announcement of a new proposed Waters of the United States rule, National Association of Manufacturers President and CEO Jay Timmons released the following statement:

“Manufacturers thank EPA Administrator Lee Zeldin for listening to the concerns of our industry and revising the definition of the Waters of the United States rule to bring certainty and predictability.

“For too long, the regulatory structure under the WOTUS rule, which often has included shifting and unclear definitions, has created legal uncertainty for manufacturers in the U.S., undermining our ability to invest and build across the country. Understanding which bodies of water require federal oversight under the Clean Water Act is critical for manufacturers planning new projects.

“Manufacturers have spent decades calling for a durable, practical approach to WOTUS—one that provides clear permitting standards and supports our industry’s commitment to environmental stewardship.

“Even after the Supreme Court’s decision in Sackett v. EPA, which established a narrower definition for bodies of water that fall under federal jurisdiction, the EPA’s 2023 rule unnecessarily rewrote critical permitting standards, overlooked substantial public input and failed to fully reflect the Court’s guidance.

“Manufacturers appreciate Administrator Zeldin’s leadership in advancing this proposal, which provides a definition that is more consistent with the law and that better serves manufacturers and the communities we support across America. We look forward to working with the agency to achieve a strong final rule for manufacturers.”

Background

In December 2024, the NAM, along with more than 100 manufacturing associations, sent a letter to President Donald Trump laying out a roadmap for regulatory actions that would boost the manufacturing economy, including revising the WOTUS rule. The NAM also called for changes to WOTUS in recommendations submitted to the Office of Management and Budget in April.

The NAM has long argued against a more expansive interpretation of WOTUS. The NAM submitted multiple sets of comments regarding the 2015 WOTUS rule to better inform policymakers. During President Trump’s first term, the NAM supported the 2017 executive order instructing the EPA to rescind the rule, and the NAM Legal Center had been in active litigation against the rule starting in 2015. The legal battle included a unanimous victory for the NAM at the U.S. Supreme Court on a key procedural issue, and in 2019, federal judges invalidated the rule.

In 2019, former EPA Administrator Andrew Wheeler and former Assistant Secretary of the Army for Civil Works R.D. James joined Timmons at NAM headquarters to announce the finalization of a rule to repeal the 2015 WOTUS rule and clear the way for a new rule to protect America’s water resources without overstepping the bounds of the law.

In 2022, the Biden administration revised the 2019 rule. The rule was again revised following a Supreme Court decision in Sackett v. EPA in 2023 that narrowed the jurisdiction of the Clean Water Act and all regulations within its authority.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

733 10th St. NW, Suite 700 • Washington, DC 20001 • (202) 637-3000

Timmons: America Runs on Coffee—and Critical Manufacturing Inputs

Washington, D.C. – National Association of Manufacturers President and CEO Jay Timmons issued the following statement on the latest trade deals.

“Today, President Trump, Secretary Bessent and Ambassador Greer delivered a major win for the American people with trade deals that keep the products that power daily life—like coffee, bananas and cocoa—affordable for working families and manufacturers. That’s something to celebrate. Today’s announcement will empower companies in the food and beverage supply chain to bring certain critical ingredients and inputs to the United States in order to enable and expand production at home.

“The U.S. is the strongest manufacturing power in the world, and thanks to this administration, manufacturers have made bold investments to enhance our ability to produce the essential inputs on our own shores. But just as coffee primarily must be produced elsewhere, the same is true for a range of critical manufacturing inputs and machinery that keep our factories humming and determine whether the next manufacturing dollar is spent in America. Americans run on coffee—and America’s manufacturers run on indispensable materials, machinery and equipment.

“We’ve had productive conversations with the administration about applying this principle, using the NAM’s U.S. Manufacturing Investment Accelerator Program, to essential manufacturing inputs—such as the critical minerals, industrial machinery and materials that drive our economy and strengthen our long-term ability to make more things in America.

“Even at full industrial capacity, the U.S. can only produce about 84% of the inputs manufacturers need—meaning at least 16% must be imported for us to build more here at home. That’s why we’ve offered practical, pro-growth solutions that allow manufacturers to bring in non-domestically produced inputs without adding new cost burdens—while rewarding companies that invest, expand and create jobs in America.

“Manufacturers are expanding capacity in America, and increasing domestic production will strengthen our industrial base and our national security. But tariffs on essential manufacturing inputs raise costs on factory floors, slow investment in new equipment and risk undercutting the president’s efforts to boost U.S. manufacturing output and jobs.

“The president’s tax, regulatory and energy dominance agendas are designed to stimulate manufacturing investment and job creation here in America. Empowering manufacturers to bring needed inputs, equipment and machinery to America’s shores would supercharge that investment, ensure the success of the president’s agenda and bring new prosperity and opportunity to communities from coast to coast.”

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Manufacturers Mourn the Passing of Former Vice President Cheney

Washington, D.C. – National Association of Manufacturers President and CEO Jay Timmons released the following statement on the passing of former Vice President Dick Cheney:

Photo Credit: Ian Wagriech, National Association of Manufacturers

Former White House photographer and NAM Director of Photography Dave Bohrer interviews Vice President Cheney at the NAM board meeting in September 2018.

“With a career in public service that spanned decades, Vice President Cheney demonstrated an unwavering commitment to those values that have made America exceptional and that manufacturers strive to advance: free enterprise, competitiveness, individual liberty and equal opportunity.

“Chief of staff under President Ford and a six-term congressman during the Reagan Revolution, he was a power player during some of the most consequential times in Washington. Our defense secretary during the Gulf War and a calm presence during 9/11, he was guided by a sense of duty to keep America safe—because America was a nation and idea worth protecting. A patriotic citizen, he lent his voice to the cause of family equality and in defense of our very democracy.

“Vice President Cheney believed that America was a force for good. He once wrote, ‘There is no other like us. There never has been.’ And indeed, there is no other like Dick Cheney. There never has been. Our deepest condolences to Lynne, Liz, Mary and their entire family.”

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

733 10th St. NW, Suite 700 • Washington, DC 20001 • (202) 637-3000

How Thermo Fisher Uses Automation to Strengthen U.S. Supply Chains

Thermo Fisher Scientific’s brand-new facility in Mebane, North Carolina, represents a big step forward for medical supply chains in the U.S.—and it’s all thanks to cutting-edge automation, overseen by workers drawn from one of the country’s hotspots for medical manufacturing talent.

The big numbers: The facility, whose grand opening was attended by North Carolina Gov. Josh Stein in August, is capable of producing an impressive 40 million precision pipette tips per week—crucial components that enable precise liquid handling in everything from clinical diagnostics to pharmaceutical research.

- The facility will create more than 100 jobs in total, including many highly skilled (and paid) automation engineer positions.

- The opening follows Thermo Fisher’s announcement earlier this year that it would commit $2 billion in investments in its U.S. manufacturing capabilities over the next four years.

The post-COVID-19 landscape: The company started working on the Mebane project after the COVID-19 pandemic, during which there was a shortage of tips, said Thermo Fisher President of Laboratory Chemicals and Laboratory Plastic Essentials Erica Hirsch.

- Thermo Fisher worked with the Department of Health and Human Services and other agencies to understand the problem with the domestic supply chain, she said.

- The answer? The company would need to invest in high-quality automation tip manufacturing, which could be scaled up as needed—especially important in the case of another pandemic.

The automation: As Thermo Fisher had learned from its operations at other facilities, the best plan for tip manufacturing is to focus on automation.

- Automation is essential to ensure consistent quality and reproducibility, not to mention a high volume of production, said Hirsch.

- The Mebane facility was a “dream opportunity,” she said, to create a highly automated facility from the ground up, instead of adding automation to an existing facility.

- The standards were high: the production lines have little direct human involvement, again to ensure every tip is as precisely engineered as possible. Each line is managed by a highly skilled technician.

The big picture: The COVID-19 pandemic also taught the company the importance of shoring up domestic supply chains and building in redundancy. In fact, said Hirsch, having redundant facilities in every region in the world has become a priority, both due to the lessons of the pandemic and to rising geopolitical tensions.

- The company has more than 7,800 workers in North Carolina, one of its major bases of operations in the U.S. Its North Carolina facilities do everything from conducting clinical research and producing pharmaceuticals to manufacturing laboratory products.

Workforce: Hirsch emphasized the close relationship that Thermo Fisher has with local trade schools and colleges, ensuring it can staff advanced manufacturing facilities like the one in Mebane.

- The company works to recruit locally and has many apprenticeship programs, including for the automation engineers at the Mebane plant.

- Mold and machine makers are also high on its list of skilled workers to train, through apprenticeships, internships and more.

- “We need to make sure we have a skilled workforce, and a workforce that spans all stages of careers,” said Hirsch.

AI: With AI on the industry’s mind, Thermo Fisher is leading the pack in integrating AI tools into all its processes, including at Mebane.

- Earlier this month, Thermo Fisher announced a partnership with OpenAI that focuses on accelerating scientific innovation, enhancing productivity and reducing complexity. As part of the collaboration, Thermo Fisher is embedding OpenAI Application Programming Interfaces into critical areas of its business—ranging from product development, service delivery, customer engagement and operational efficiency.

- AI will be critical for Mebane as it is a highly automated, data-driven facility, said Hirsch.

Looking ahead: Thermo Fisher continues to be committed to offering products that combine high-quality scientific expertise with industry-leading technologies, helping its customers to accelerate life-sciences research and develop new therapies for patients who are waiting, said Hirsch.

- “The company’s mission—to enable its customers to make the world healthier, cleaner and safer—fuels the passion of its colleagues and drives the many contributions they make each day,” she added.

Photo credit: Office of Governor Josh Stein

New NAM Roadmap Ties America’s AI and Energy Future to Urgent Need for Permitting Reform

WASHINGTON, D.C.— The National Association of Manufacturers today released Manufacturing’s Roadmap to AI and Energy Dominance, a blueprint outlining the steps policymakers must take to strengthen America’s energy and artificial intelligence dominance—including comprehensive permitting reform.

Manufacturers are leading the way—integrating AI into every part of their operations, from product design, to shop floor operations, to supply chain management. More than half of manufacturers (51%) already use AI, and 80% say it will be essential to grow or even maintain their business by 2030, according to the Manufacturing Leadership Council, the digital transformation division of the NAM.

The roadmap lays out principles that will advance U.S. energy production and, in turn, unlock the full potential of AI. AI is transforming manufacturing—but without abundant, affordable energy and a resilient and reliable power grid, America risks falling behind. AI-powered modern manufacturing depends on an ambitious energy and innovation policy framework—which can be achieved in part by reforms to America’s broken permitting system.

“Manufacturing sits at the crossroads of America’s energy dominance, AI leadership and the strength of our power grid,” said NAM President and CEO Jay Timmons. “If America wants to win the global race for AI, we must first win on energy. That means advancing the administration’s goals for energy dominance—through bipartisan, comprehensive permitting reform, modernized infrastructure and an all-of-the-above energy strategy that allows manufacturers to innovate, build and grow right here at home.”

AI-powered manufacturing depends on forward-looking energy and innovation policies. Policymakers must do the following:

- Reform America’s broken permitting process to get shovels in the ground faster—with fewer delays and less uncertainty. Eighty percent of manufacturers say that the length and complexity of the permitting process is harmful to increasing investment.

- Bolster American energy dominance. America’s energy demand is surging—and the pace isn’t slowing. Manufacturers need to be able to produce and use every energy source available to meet this critical moment. Ninety-four percent of manufacturers support permitting reforms around the buildout of energy generation, infrastructure and products.

- Ensure a reliable, resilient and affordable grid that can power manufacturing growth and data center operations. Eighty percent of manufacturers want the Trump administration to work with Congress to deliver comprehensive permitting reform legislation to increase energy generation and grid modernization to supply the energy needed to power both AI growth and traditional manufacturing.

- Strengthen American AI leadership by fostering innovation and preventing regulatory overreach. Eighty-seven percent of manufacturers say it is important for lawmakers to understand how manufacturers use AI.

Read the full roadmap here.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Manufacturers Talk Talent Development at the MI’s Workforce Summit

In an ever-changing world, collaboration is more necessary than ever for solving the challenges facing our manufacturing workforce. Last week, in Charlotte, North Carolina, the Manufacturing Institute’s annual Workforce Summit united more than 300 industry leaders to do just that, tackling workforce challenges while redefining what manufacturing represents for tomorrow.

The backdrop: MI Chief Program Officer Gardner Carrick opened the summit by highlighting a shift in public perception. Americans view manufacturing more positively now, and attitudes toward education and career pathways are evolving. As confidence in the value of a traditional four-year degree declines, new opportunities are emerging for skills-based careers in modern manufacturing.

- But, Carrick noted, the industry must stay on the offensive. “The next generation of workers doesn’t need convincing that technology is exciting; they live it,” he said.

- “The story isn’t that we’ve changed; it’s that we’re leading,” Carrick concluded. “And that’s what will inspire the next generation.”

Quick insight: Participants at the summit, who came from dozens of manufacturing sectors and many nonprofit and partner organizations, discussed practical, transformative solutions in every session. Here are some of the big takeaways:

- Rethink education: ABB’s Jason Green emphasized the need to get technology into the hands of students early and to reimagine career and technical education, including real-world learning and applications. Apprenticeships built on company needs can help create talent pipelines that are both practical and custom-fit.

- Invest in culture: Lisa Winton of Winton Machine explained why she views culture as a competitive advantage, especially for small manufacturers. Her team leverages local training resources and encourages multigenerational learning, where mentorship flows both ways.

- Design for flexibility: Amatrol’s Paul Perkins urged companies to mold jobs around people, not the other way around. By creating fluid career paths and removing unnecessary barriers, manufacturers can use mobility itself as an attraction strategy.

- Focus on skills: Walmart.org’s Sean Murphy and the MI’s Sytease Geib highlighted skills-based strategies that strengthen pipelines, accelerate and validate learning, enhance retention and unlock meaningful career growth.

- Empowering the frontline: Jerry Dolinsky, CEO of Dozuki, and Dr. Rebecca Powers Teeters of 3M highlighted how AI-driven digital tools can help frontline workers. Connected workers can bridge skills gaps, boost engagement and drive productivity, while practical AI applications create smarter workflows, enhance safety and foster continuous learning and innovation.

Parting words: “The momentum, the environment, the atmosphere surrounding what we do will continue to evolve, and we know that we can solve our problems if the industry is tackling them together,” said MI President and Executive Director Carolyn Lee. “The MI will continue to be here to support you.”

Couldn’t make it this time? The MI, the NAM’s 501(c)3 workforce development and education affiliate, works year-round to help companies strengthen their workforce and deliver innovative solutions to workforce challenges. Here are some ways to get involved:

- Sign up for updates to the MI’s Solutions Center for resources, best practices and opportunities to learn from peers through the Solutions Series. Explore our regularly scheduled virtual convenings as part of the Solutions Series to see how manufacturers across the country are addressing workforce challenges.

- Get updates directly from the MI on the latest workforce insights and be among the first to receive information about upcoming events and to register for next year’s Workforce Summit, taking place in Indianapolis, Indiana.

- Want more labor data and insights? Sign up for the MI’s comprehensive Workforce in Focus newsletter to stay up to date on the latest workforce trends.

Single-Family Home Sales Rise, Condos and Co-Ops Remain the Same

Existing home sales increased 1.5% in September and 4.1% over the year. Housing inventory stepped up to 1.55 million units, reflecting a 1.3% rise from August and 14.0% jump from last year. The median existing home price was $415,200, up 2.1% from last year. The Northeast, South and West posted monthly increases in existing home sales, while the Midwest registered a decline in September.

Single-family home sales rose 1.7% from August and 4.5% from September 2024, with the median price increasing 2.3% from last year to $420,700. Condo and co-op sales stayed the same over the month and over the year at 370,000 units in September. Meanwhile, the median price for condos and co-ops edged down 0.6% from the prior year to $360,300.

Homes were typically on the market for 33 days in September, up from 31 days in August and 28 days in September 2024. First-time buyers made up 30% of sales in September, up from 28% in July and 26% in September 2024.

Manufacturing Activity Advances to a Two-Month High

The S&P Global Flash U.S. Manufacturing PMI rose from 52.0 to 52.2 in October, a two-month high. This continues the trend in business conditions with nine of the past 10 months signaling growth. Factory production grew for the fifth consecutive month, while new orders increased at the steepest pace in one-and-a-half years, driven by the domestic market. On the other hand, export orders for manufactured goods fell at the fastest rate since February, with sales to China and Europe falling.

Inventories continued to grow, but only marginally, as declining backlogs caused manufacturers to reduce input buying in October. Meanwhile, supplier delivery times shortened compared to September. Manufacturers’ input cost inflation increased at the slowest pace since February but remained incredibly high and continued to be attributed to tariffs. Selling prices for goods accelerated in October but stayed below rates seen in the preceding six months. Firms continued to report difficulties passing higher costs on to customers due to suppressed demand and increased competition.

Overall business activity advanced to a three-month high, increasing from 53.9 in September to 54.8 in October. This reading is accompanied by the largest rise in new business seen in 2025, with both the service sector and manufacturing experiencing growth in business activity in October. Overall, new order growth rose at the steepest level so far this year despite service exports falling. Despite price increases in manufacturing, service sector inflation eased in October.

Meanwhile, optimism about future business conditions fell in October, amid continued uncertainty around trade policy and the ongoing federal government shutdown. Manufacturing optimism declined to the second lowest level since June 2024 despite continued hope that tariffs could stimulate domestic production in the coming year.