Q&A with Sen. Daines on the Pass-Through Deduction

NAM: Sen. Daines, H.R. 1 permanently extended the Section 199A pass-through deduction, preventing the substantial tax increase that would have hit small manufacturers at the start of 2026. You have been among the Senate’s most persistent champions of pass-through businesses since the Tax Cuts and Jobs Act was enacted. What does achieving permanency mean for small manufacturers in Montana and across the country?

Sen. Daines: Our small businesses and manufacturers are the backbone of our country’s economy, driving growth and investment across states like Montana. Since I entered Congress, I prioritized the need to protect this industry and warned of what a less competitive America looks like.

I championed the small business deduction in 2017, and last year, I led the charge on making sure this and other pro-growth provisions became permanent. Clarity and certainty are two of the most important things these job creators need to be as successful as possible, and making 199A permanent delivered both.

NAM: You introduced the Main Street Tax Certainty Act specifically to make the 199A deduction permanent. H.R. 1 accomplished that goal. How did your legislation and sustained advocacy help build the political and policy case for permanency in the reconciliation package, and were there particular provisions in the final bill—beyond the basic permanency—that reflect your priorities for pass-through manufacturers?

Sen. Daines: As important as it was to make sure this provision was included in 2017, it was imperative we avoided the steep tax increase small businesses and manufacturers faced if we let this expire. Since the day the TCJA was signed into law, we pushed to make this provision permanent. Businesses from every state came in and helped us tell the story of what this means for them. When the time came to draft the Working Families Tax Cuts, the Main Street Tax Certainty Act was one of the most co-sponsored bills in the Senate. We had nearly all Republican senators on that bill advocating for its inclusion in final passage, and we achieved exactly that.

NAM: The Senate Finance Committee conducted detailed working group discussions ahead of H.R. 1. What arguments proved most decisive in the Senate debate over 199A permanency, and are there remaining gaps or unresolved issues in the tax treatment of pass-through manufacturers that you believe should be addressed in future legislation?

Sen. Daines: Good policies are easy to defend, and the economic data behind 199A spoke for itself. Pass-through businesses employ more than half of private–sector workers, [and] more than 96% of businesses in our country are organized as pass-throughs. The deduction itself is directly responsible for 2.6 million jobs and $325 billion of the United States’ GDP. Many of these businesses are manufacturers who are the backbone of our competitiveness. A successful manufacturing industry supports the American economy and helps protect us against foreign adversaries.

NAM: Manufacturers appreciate your passion and persistence in securing the 199A deduction for the long term. What can our members do to help ensure the benefits of this provision reach every small manufacturer across the country?

Sen. Daines: We can see economic data and how policies will broadly operate, but hearing firsthand from businesses [that] have utilized those policies to reinvest and grow makes all the difference. We wouldn’t have been able to get nearly our entire conference onto the Main Street Tax Certainty Act if we didn’t have stories from each state to point to.

Q&A with Rep. Carol Miller on Tax Certainty

NAM: Rep. Miller, H.R. 1 has been signed into law, preserving the 21% corporate tax rate established by the 2017 Tax Cuts and Jobs Act. As the leader of the House Ways and Means Supply Chain Tax Team leading up to the bill’s passage, what does preserving this rate on a permanent basis mean for manufacturers’ ability to invest in American supply chains and compete globally?

Rep. Miller: Tax certainty is essential to maintaining the United States’ position as a global leader in manufacturing. The Working Families Tax Cuts will deliver meaningful relief to American manufacturers, driving the development of new facilities, the creation of jobs and increased investment across the country. The Ways and Means Supply Chain Tax Team focused on advancing pro-growth policies to fuel long-term economic prosperity. Key provisions in the legislation—including permanent research and development expensing, full immediate expensing, a strengthened interest deduction and a 100% factory construction deduction—provide businesses with the certainty and incentives needed to plan, invest and compete globally.

NAM: With the 21% corporate rate now secured through H.R. 1, U.S. manufacturers have a more competitive tax foundation than they did even a year ago. But the global tax landscape continues to shift, with major trading partners and competitors making their own adjustments to attract investment and manufacturing activity. From your vantage point leading the Supply Chain Tax Team, how has that preservation of the 21% corporate rate bolstered the United States’ position in promoting and attracting investment?

Rep. Miller: The preservation of the 21% corporate rate is critical in promoting American manufacturing because companies can invest in expanding infrastructure, purchase new equipment and increase workforce without tax liability uncertainty. The Working Families Tax Cuts compounded with bonus depreciation and immediate research expensing have proved to be effective for the industry, and we will continue to advocate for pro-growth policy, which leads to new markets and more opportunities.

NAM: Your Supply Chain Tax Team has traveled the country meeting with manufacturers since the TCJA was enacted. Now that H.R. 1 is law, what are businesses in your district or on your tax team’s radar telling you about specific investments or hiring decisions they are making or accelerating because the 21% corporate rate is no longer at risk?

Rep. Miller: The real-world impact of the Working Families Tax Cuts has been clear and meaningful, reinforcing the need for stable, pro-growth tax policy to help American manufacturers succeed. In my home district, we’ve seen these policies translate into new factories, new jobs and expanded opportunities. Companies like Conn-Weld Industries and Ferroglobe have used this tax relief to invest in their operations, grow their businesses and strengthen the local economy.

NAM: Thank you for your leadership in protecting manufacturers through H.R. 1. What should NAM members be doing now to help communicate the benefits of the 21% corporate rate and to support continued pro-manufacturing tax policy?

Rep. Miller: NAM members should share their stories and voice their support for the Working Families Tax Cuts and communicate the real-world impact this legislation has on the country, their business and the employees and their families who benefit. Manufacturers are at the core of our economy and need a predictable and pro-growth tax code.

Q&A with Sen. Young on R&D Expensing

NAM: Sen. Young, H.R. 1 restored immediate domestic R&D expensing, ending the amortization requirement that had been in effect since 2022. You have been one of the Senate’s most dedicated champions of R&D competitiveness through the American Innovation and Jobs Act. How did your years of sustained advocacy help deliver this outcome in the final reconciliation package?

Sen. Young: The American Innovation and Jobs Act laid the foundation for a multiyear, bipartisan effort to restore full and immediate expensing. From the outset, our goal was to make clear that strong R&D incentives are essential to maintaining America’s competitive edge. With the support of my Senate Finance Committee colleagues and active industry partners like the NAM, we built a broad coalition that understood the real-world consequences of the amortization treatment. This sustained advocacy was critical to ensuring this policy was included in the final version of the One Big Beautiful Bill Act.

NAM: The amortization requirement that was in effect from 2022 to 2024 was particularly damaging for manufacturers, who conduct 52% of private-sector research. Now that immediate expensing is restored and prior-year costs can be accelerated, what are Indiana manufacturers or other stakeholders telling you about how this relief changes their investment and hiring plans?

Sen. Young: During the three-year span when businesses had to amortize, I heard from countless Hoosier employers, including many in the manufacturing and life sciences industries, about how the R&D tax treatment was forcing incredibly difficult decisions. These included delaying R&D projects, scaling back hiring for key personnel like engineers and scientists and, in some cases, even considering shifting research activity overseas. That kind of uncertainty is especially challenging for industries that rely on long-term investment cycles.

Now that immediate expensing has been restored, and restored on a permanent basis, there is a renewed sense of confidence. Businesses back home have shared with me that they are moving forward with previously delayed investments, expanding their research operations and accelerating plans to grow their workforce. Those are the types of business decisions we should be encouraging in our tax code.

NAM: Restoring R&D expensing is a major step, but the United States still trails competitors like China in the overall generosity of R&D incentives. What is your honest assessment of where America now stands in the global innovation competition, and what further actions—whether through additional tax policy, increased federal R&D investment or streamlined regulatory pathways—should Congress prioritize to ensure the U.S. remains the world’s leading destination for manufacturing innovation?

Sen. Young: As our global competitors, like China, are expanding their R&D incentives, we simply cannot allow our nation and our economy to fall behind. To remain the world’s leading destination for innovation and advanced manufacturing, we need a more comprehensive approach. That includes increasing federal investment in critical research areas, ensuring our regulatory environment supports the commercialization of new technologies and strengthening workforce development and apprenticeship streams so that we can better connect students and workers to high-demand careers in manufacturing and innovation.

My focus going forward is on advancing policies that not only restore our competitiveness but position the United States to lead in rapidly growing industries like advanced manufacturing, artificial intelligence, quantum and biotechnology.

NAM: Thank you, Sen. Young. What can NAM members do to help manufacturers take advantage of the restored R&D deduction and to support continued investment in American manufacturing innovation?

Sen. Young: I would encourage NAM members to continue engaging with policymakers and sharing examples of how R&D incentives are driving investment, hiring and innovation in their communities. Those real-world stories about the advancements companies are making are incredibly important as we consider future policy decisions.

I’d also urge manufacturers to fully utilize the restored deduction and continue investing in their workforce and research capabilities. By doing so, and by staying engaged in the policymaking process, you can help ensure we build on this progress and continue strengthening America’s leadership in manufacturing.

Sen. Young on Championing Immediate R&D Expensing Provision for Manufacturers

Marking the approach of H.R. 1’s first anniversary this July, the NAM is highlighting the law’s pro-manufacturing tax wins. This week, we spoke to Sen. Todd Young (R-IN), a leading proponent of immediate R&D expensing, which the law successfully restored.

How they did it: When asked about his efforts to get this key provision reinstated, Sen. Young said, “From the outset, our goal was to make clear that strong R&D incentives are essential to maintaining America’s competitive edge.”

- “With the support of my Senate Finance Committee colleagues and active industry partners like the NAM, we built a broad coalition that understood the real-world consequences of the amortization treatment.”

Making a difference: “During the three-year span when businesses had to amortize, I heard from countless Hoosier employers, including many in the manufacturing and life sciences industries, about how the R&D tax treatment was forcing incredibly difficult decisions,” said Sen. Young. “These included delaying R&D projects, scaling back hiring for key personnel like engineers and scientists and, in some cases, even considering shifting research activity overseas.”

- “Now that immediate expensing has been restored, and restored on a permanent basis, there is a renewed sense of confidence,” he continued. “Businesses back home have shared with me that they are moving forward with previously delayed investments, expanding their research operations and accelerating plans to grow their workforce.”

Why it matters: “As our global competitors, like China, are expanding their R&D incentives, we simply cannot allow our nation and our economy to fall behind,” said Sen. Young.

- “My focus going forward is on advancing policies that not only restore our competitiveness but position the United States to lead in rapidly growing industries like advanced manufacturing, artificial intelligence, quantum and biotechnology.”

Advice for manufacturers: When asked what manufacturers should do now that immediate R&D expensing has been made permanent, Sen. Young said, “I would encourage NAM members to continue engaging with policymakers and sharing examples of how R&D incentives are driving investment, hiring and innovation in their communities. Those real-world stories about the advancements companies are making are incredibly important as we consider future policy decisions.”

- “I’d also urge manufacturers to fully utilize the restored deduction and continue investing in their workforce and research capabilities. By doing so, and by staying engaged in the policymaking process, you can help ensure we build on this progress and continue strengthening America’s leadership in manufacturing.”

Read the whole thing: You can read the whole Q&A here.

Q&A with Sen. Lankford on Tax Policy

NAM: Sen. Lankford, H.R. 1 permanently restored 100% bonus depreciation for qualifying property acquired after Jan. 19, 2025, reversing a phasedown that had reduced the deduction to 40% in 2025 and would have eliminated it by 2027. As a member of the Senate Finance Committee, what does permanent full expensing mean for manufacturers making long-lived capital investment decisions, and how does permanency change their planning horizon relative to a temporary extension?

Sen. Lankford: Permanency is the difference between short-term tax relief and long-term economic certainty. Manufacturers are not making one-year decisions. They are making 10-, 20-, even 30-year capital allocation decisions on facilities, heavy equipment and production lines. When full expensing is temporary or phasing down, it distorts those decisions and often forces companies to either accelerate investments inefficiently or delay them altogether.

By making 100% expensing permanent, we are giving manufacturers confidence that the tax treatment will be consistent across the full lifecycle of an investment. That stability lowers the cost of capital, improves after-tax returns and allows companies to plan rationally instead of reacting to arbitrary deadlines.

That is why I have pushed for permanency through efforts like the ALIGN Act, which was included in the Working Families Tax Cuts Act, because pro-growth policy only works if businesses can rely on it over the long term.

NAM: During the phasedown years, when bonus depreciation fell from 100% to 80% to 60% to 40%, manufacturers reported delaying or canceling major capital purchases because the economics no longer worked as favorably. Now that 100% expensing is restored permanently, what evidence are you seeing—in Oklahoma or nationally—that manufacturers are moving forward on investments that were on hold?

Sen. Lankford: What we are hearing, both in Oklahoma and across the country, is that the return to full expensing is beginning to unlock projects that were sitting on the sidelines. During the phasedown, when expensing dropped from 100% to 40%, many of those investments simply didn’t pencil out.

That lines up with what we know about Oklahoma’s economy. The state is heavily concentrated in capital-intensive sectors like oil and gas, manufacturing and aerospace. Oil and gas alone accounts for a significant share of state GDP, and when you include the broader supply chain, it touches more than a quarter of the economy. These are exactly the types of industries where cost recovery drives investment decisions.

In practical terms, that showed up in delayed energy projects, deferred equipment purchases and slower expansion of processing and manufacturing facilities. In manufacturing and aerospace, companies stretched the life of existing equipment and postponed automation upgrades.

Now, with full expensing permanently restored, those same businesses are revisiting projects. That includes moving forward on pipeline investments, placing new equipment orders and advancing plant and infrastructure upgrades. The key shift is that companies are no longer trying to time the tax code. They are making decisions based on operational need and long-term growth.

NAM: H.R. 1 also raised the Section 179 expensing cap from $1 million to $2.5 million, providing a complementary benefit particularly for smaller manufacturers. The legislation also expanded bonus depreciation to manufacturing facilities. How do bonus depreciation, the enhanced Section 179 and the new deduction for factories work together to drive capital investment across manufacturers of all sizes, and what are you hearing from businesses about how these provisions are impacting them?

Sen. Lankford: For smaller and mid-sized manufacturers, Section 179 is often the tool they use the most. These are businesses that are upgrading equipment, adding a new machine or expanding part of their shop floor. They are not doing massive projects all at once. They need something simple, predictable and easy to use. Increasing the cap means more of those everyday investments can be written off immediately, which helps with cash flow and makes it easier to keep reinvesting.

For larger manufacturers, the scale is different. They are looking at bigger equipment purchases, full production lines and major upgrades across facilities. Bonus depreciation matters here because it allows them to expense those larger investments upfront. When you are talking about large equipment investments, that timing difference can influence whether a project moves forward now or gets pushed out.

The addition of expensing for manufacturing facilities is a big step forward. For a lot of companies, the building is one of the most expensive parts of the project, not just the equipment inside it. Whether it is a new plant or expanding an existing one, being able to expense both the facility and the equipment reflects the full cost of what it takes to grow.

When you put all of that together, it creates a system that works for manufacturers at different sizes and at different stages. It supports the smaller, steady investments and the larger, long-term projects. It does not solve every challenge, but it removes a major barrier and lets companies make decisions based on what they actually need to grow.

NAM: Thank you, senator. What can NAM members do to help manufacturers understand and act on the restored bonus depreciation and enhanced Section 179 provisions?

Sen. Lankford: The most important thing NAM members can do is make sure permanent expensing actually reaches the shop floor. A lot of small manufacturers may not have heard about what changed, and even if they have, they may not immediately connect a tax provision to a real equipment decision. It’s a simple but important message: if you’ve been holding off on a new piece of equipment, talk to your accountant now, because you may be able to write off the full cost this year. Pro-growth policy only delivers if manufacturers know about it and use it, and that’s where NAM can make a real difference. That’s what will drive long-term investment, create jobs and grow local economies.

On Tax Day, the Receipts Are Filled with Manufacturing Wins

Washington, D.C. – On the first Tax Day since passage of H.R. 1, National Association of Manufacturers President and CEO Jay Timmons released the following statement:

“This Tax Day, manufacturers now have a permanent, pro-growth tax code that allows our industry to compete and win. Thanks to President Trump, leaders in his Cabinet and in Congress, the 2017 provisions of the Tax Cuts and Jobs Act were not just made permanent—they were made even stronger, which saved 6 million jobs. The tax and investment incentives in H.R. 1 amount to the most significant economic transformation in the history of our industry, serving as rocket fuel for manufacturers.

“Manufacturers’ optimism is on the rise, and they are ready to keep building, investing and leading—but that requires certainty across the board to take full advantage of H.R. 1’s transformative provisions. President Trump and Congress went above and beyond to deliver tax certainty for manufacturers, and we look forward to continuing to work with them to build on this progress—ensuring certainty and lowering the cost of doing business—so that manufacturers can deliver the greatest manufacturing era in American history.

“This Tax Day, the message is clear: when Washington gets the tax code right, manufacturers deliver.”

This week, Timmons published a joint op-ed in the Washington Examiner with House Majority Whip Tom Emmer (R-MN) on the pro-growth tax reforms of H.R. 1. Read it here.

Manufacturing Wins

Learn more about how tax reform is bolstering manufacturing in America:

- Ketchie CEO Credits Trump’s “Beautiful Bill” with Helping Her Machine Shop Prosper

- Brunswick Revs the Engine on Innovation and U.S. Investment

- Tax Reform Delivers “Biggest Investment in Company History” for Marlin Steel

- J&J Makes Major Investment in North Carolina Thanks to Tax Reform

- Sylvamo to Congress: Tax Reform Made Manufacturing Success Possible

Background

Prior to final passage of H.R. 1 in 2025, the NAM activated manufacturers in America—engaging shop floor workers, plant managers, executives and state and local partners nationwide—as part of the “Manufacturing Wins” campaign. With a coordinated public advocacy campaign, which included outreach to congressional offices both in district and in Washington, targeted social media drives, video testimonials and local media op-eds, the NAM made the case for this bill directly to members of Congress and the American people. These collective voices underscored how preserving and expanding key tax provisions translates into growing businesses, creating jobs and powering stronger communities.

In January 2025, the NAM released a landmark EY study on the economic consequences of failing to renew the pro-manufacturing provisions of the Tax Cuts and Jobs Act. The NAM was joined by Senate Finance Committee Chairman Mike Crapo (R-ID), House Ways and Means Committee Chairman Jason Smith (R-MO) and House Majority Leader Steve Scalise (R-LA) for a Capitol Hill press conference highlighting the study.

KEY FACTS: If Congress had failed to preserve tax reform in 2025, the U.S. would have risked:

- 5.9 million lost jobs;

- A $540 billion reduction in employee compensation; and

- A $1.1 trillion shortfall in U.S. GDP.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Timmons: “A Leader of Substance and Integrity”—NAM Congratulates Jim Fitterling on Executive Chair Role at Iconic Manufacturer Dow

Washington, D.C. – National Association of Manufacturers President and CEO Jay Timmons issued the following statement congratulating former NAM Board Chair Jim Fitterling on his appointment as executive chair of the board of Dow Inc.

“Dow’s announcement marks an important leadership transition for the iconic manufacturer and an opportunity to recognize the extraordinary leadership of Jim Fitterling.

“Jim is a leader of substance and integrity—clear in his direction, consistent in his approach and deeply committed to the people and communities that power manufacturing. As NAM Board chair, he helped strengthen the association’s impact and build consensus across the industry around a competitiveness agenda that is delivering results—from historic tax reform implementation to regulatory modernization and a growing consensus around permitting reform as essential to unlocking investment, jobs and growth in America.

“Jim’s imprint on America’s future has extended well beyond policy. He has been a driving force behind efforts to inspire the next generation of manufacturers. Through his leadership, the Creators Wanted campaign became the most successful workforce initiative in modern manufacturing history—reaching millions of students, parents and educators and changing perceptions about careers in our industry. He approached that work with a straightforward message: if you want to design, build and create, manufacturing offers that opportunity.

“He carried that same commitment into his strong support for the Manufacturing Institute as a respected advocate for bringing one’s authentic self to the workplace, helping broaden the impact of the MI in developing talent and opening doors for more Americans to pursue careers in modern manufacturing.

“Jim leaves behind a stronger Dow, a more competitive manufacturing industry and meaningful progress in building the workforce that will define the future of manufacturing in the United States. On a personal level, he has been a trusted partner, counselor and a leader who consistently pushed for excellence and results on behalf of manufacturers.

“As we continue our historic charge with Jim as an Executive Committee member of the NAM, manufacturers congratulate Karen Carter on being named CEO of Dow. Karen is a proven and accomplished leader, and we look forward to working with her as she builds on Dow’s momentum and continues advancing manufacturing in the United States and around the world.”

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org

733 10th St. NW, Suite 700 • Washington, DC 20001 • (202) 637-3000

ICYMI: Iowa Manufacturer Expands, Credits Pro-Growth Tax Law

Vermeer Corporation Announces Plan to Build New Facility, Create 300+ Jobs

Washington, D.C. – Vermeer Corporation, an industrial and agricultural equipment producer based in Pella, Iowa, is crediting the pro-growth tax provisions of H.R. 1 with supporting the company’s plan to build an all-new 300,000-square-foot facility in the Des Moines metro that will create more than 300 jobs.

Vermeer said in a company statement, “We’re grateful for the state of Iowa, the pro-business environment, the skilled workforce here and economic policies, like Working Families Tax Cuts, that have helped support Vermeer’s long-term growth.”

Last August, National Association of Manufacturers Executive Vice President Erin Streeter joined Rep. Mariannette Miller-Meeks (R-IA) for a Made in America Manufacturing Tour across Iowa’s 1st District, where they visited Vermeer’s facility in Pella. During the tour, Vermeer President and CEO and NAM Executive Committee member Jason Andringa said H.R. 1 “sets up manufacturers for a generation of continued growth and advancement.”

Streeter praised Rep. Miller-Meeks’ leadership during the tour.

“H.R.1 is a landmark win for manufacturing—delivering pro-growth policies that will strengthen our industry for years to come. Without bold leadership from lawmakers like Rep. Miller-Meeks, manufacturers could have been crippled by the largest tax hike in history—jeopardizing the progress we made after the 2017 Tax Cuts and Jobs Act. Iowa’s 1st Congressional District is the first in the state for manufacturing. We want to thank her for protecting 13,000 jobs and $1.2 billion in wages at more than 800 manufacturing companies in her district alone.”

Background

KEY FACTS: If Congress had failed to preserve tax reform in 2025, the U.S. would have risked:

- 5.9 million lost jobs;

- A $540 billion reduction in employee compensation; and

- A $1.1 trillion shortfall in U.S. GDP.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

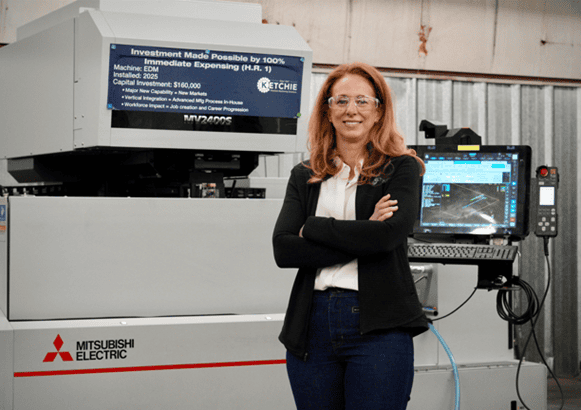

ICYMI: “Ketchie CEO Credits Trump’s ‘Beautiful Bill’ with Helping Her Machine Shop Prosper”

Washington, D.C. – As part of the 2026 National Association of Manufacturers State of Manufacturing Tour, Ketchie President and Owner Courtney Silver hosted the NAM for a discussion on how tax certainty due to the NAM-backed H.R. 1 has empowered manufacturers like her to reinvest in their workforce and facilities.

The tour stop was covered by Business North Carolina. Excerpts of the report can be found below. Bolding has been added.

—-

Ketchie CEO credits Trump’s ‘beautiful bill’ with helping her machine shop prosper

Business North Carolina

Kevin Ellis

Feb. 23, 2026

https://businessnc.com/ketchie-ceo-credits-trumps-beautiful-bill-with-helping-her-machine-shop-prosper/

Miguel Carrillo describes himself as a “machine nerd,” and he had an engaged audience on Monday watching him operate a $700,000 device brought in last year to Concord-based Ketchie, the machine shop where he works.

Ketchie may only have 20 employees, but it was a stop on the State of Manufacturing Tour that National Association of Manufacturers President Jay Timmons began last week in Cleveland and will continue across the country after visiting three Charlotte-area sites on Monday. Tagging along with Timmons at Ketchie was Acting Deputy Secretary of the U.S. Treasury Derek Theurer, U.S. Rep. Tim Moore of Cleveland County and NC Chamber President Gary Salamido.

Ketchie CEO Courtney Silver was a supporter of the “One Big Beautiful Bill,” the legislation signed into law last year by President Donald Trump. She testified at congressional hearings before its passage about how it would help small businesses. Timmons said he had heard so much about Ketchie’s new machines, he wanted to see them in action.

The tax bill that eliminates income tax on overtime and tips for some workers also allows businesses to reduce their tax bills on investments immediately, rather than spreading the reduction out over several years, says Silver.

“When you can expense an investment in the year it was purchased, it provides cash flow to companies and continues to allow them to make new investments,” says Silver.

Ketchie purchased three machines last year that combined cost more than $1.1 million, plus made about $400,000 in other investments, including AI software that has cut some hour-long processes down to five minutes.

“I would have never made those investments without immediate expensing,” Silver says. She says she’s also looking to add five workers to her shop.

“This is a perfect example of what you can do to help build America and American manufacturing with the right policies in place,” says Timmons.

Theurer said it was nice to see advanced manufacturing take place in a North Carolina factory rather than spending his day on policy in the nation’s capital.

“This type of investment is what we intended to see when we made our big tax policy and worked for smarter regulation,” said Theurer.

…

Ketchie supplies metal parts to railroad, aerospace and heavy industry manufacturers, such as Charlotte steelmaker Nucor, Davidson-based HVAC company Trane and Norfolk Southern. The company was started in 1947 by Edgar Ketchie, the grandfather of Silver’s late husband.

On Monday, Carrillo was machining a steel part needed by an industrial recycling company. The Dual Spindle 5-Axis Machining Center that Ketchie bought last year doesn’t require Carrillo to reset the machine for the other side of the metal part, which is about half the size of a deck of cards, but grooved. It means quicker production and fewer human errors, he says.

“It allows me to step out and allows the machine to do the heavy lifting,” says Carillo. The advanced manufacturing aspect attracted the 2024 graduate of A.L. Brown High School to work at Ketchie after starting in a job shadowing program while a high school junior. “It’s nice when a machine can do one thing, but it’s really nice when a machine can do a lot of things.”

…

—-

Background

Learn more about Silver’s testimony before Congress in 2025 on the importance of preserving the pro-manufacturing policies of the Tax Cuts and Jobs Act here.

KEY FACTS: If Congress had failed to preserve tax reform in 2025, the U.S. would have risked:

- 5.9 million lost jobs;

- A $540 billion reduction in employee compensation; and

- A $1.1 trillion shortfall in U.S. GDP.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

NAM Tour Highlights How Tax Reform Fuels Growth in North Carolina

2026 NAM State of Manufacturing Tour Stops in Charlotte and Concord, North Carolina

CHARLOTTE – The National Association of Manufacturers—official partner of America250—in partnership with the North Carolina Chamber, continued its 2026 NAM State of Manufacturing Tour today in Charlotte and Concord, North Carolina, under the theme “Competing for the Future.”

The tour stop highlighted how the NAM-backed H.R. 1 is creating a more competitive tax environment—and why sustaining that certainty, along with regulatory rebalancing, modern infrastructure and reliable energy, is critical to driving continued investment and job creation across the sector. Today’s visits included Ketchie Inc., Siemens Energy and Electrolux.

“Here in North Carolina, we’re seeing exactly what tax certainty makes possible,” said NAM President and CEO Jay Timmons. “Thanks to President Trump and leaders in Congress, the pro-growth provisions in H.R. 1 were made permanent and strengthened, delivering a win for manufacturers of all sizes. To make the United States the best place in the world to do business and so manufacturers across North Carolina can keep investing, hiring and competing, we must build on that tax foundation we secured. That means enacting comprehensive, commonsense permitting reform to unleash American energy dominance, driving the funding we need for strong, modern infrastructure, modernizing regulations, investing in our manufacturing workforce and implementing smart AI policy—all through a comprehensive manufacturing strategy.”

Ketchie President and Owner Courtney Silver hosted the first stop of the day with a tour and panel discussion on how tax certainty due to the NAM-backed H.R. 1 has empowered manufacturers like her to reinvest in their workforce and facilities. Silver emphasized that pro-growth tax policies, such as permanent full expensing, have enabled business owners to remain agile and competitive. With that tax certainty in place, Ketchie has invested in new critical machinery—expanding capacity, increasing efficiency and positioning the company to hire, grow and compete for the long term.

The tour then moved to Siemens Energy, which recently announced a $421 million expansion in North Carolina to grow its large power transformer manufacturing and continue gas turbine production in Charlotte—an investment expected to create 500 new jobs statewide.

The day concluded at the North American headquarters of Electrolux, the global home appliance manufacturer, employing hundreds in the Charlotte region.

Throughout the day, business leaders highlighted the impact of North Carolina’s nearly 500,000 manufacturing workers who make up more than 11% of the workforce and power the largest manufacturing sector in the Southeast.

Timmons was joined by North Carolina Chamber President and CEO Gary Salamido and other NAM leaders throughout the day. Deputy Secretary of the Treasury Derek Theurer and Rep. Tim Moore (R-NC) participated in the visit to Ketchie.

“Thanks to America First policies, domestic manufacturing is back, and we’re seeing serious investments right here in North Carolina,” said Rep. Moore. “It was great to join the National Association of Manufacturers at Ketchie alongside Deputy Secretary of the Treasury Derek Theurer to see firsthand how tax certainty and pro-growth policies are giving companies the confidence to expand and compete with anyone in the world.”

“North Carolina’s manufacturers are a major driver of our state’s economy, contributing a higher-than-average 15% of our gross state product,” said Salamido. “With a manufacturing tradition like ours, we are proud to partner with the NAM to show the nation that our state is the premier destination for manufacturing, so long as pro-business policies allow for it.”

From Charlotte, the 2026 NAM State of Manufacturing Tour will go on to Milwaukee, Wisconsin; Dallas and Houston, Texas; and Phoenix, Arizona. The tour made stops in New York City, Cleveland and Pennsylvania prior to today’s events in Charlotte. Throughout the tour, the NAM will continue meeting with policymakers, manufacturers of all sizes, students and business leaders, advocating for the people and policies that will ensure the United States is the best place in the world to do business. To learn more about the tour and the NAM’s mission, visit https://nam.org/stateofmfg/.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.