Policy and Legal

Manufacturers need smart laws and effective policies. That’s why the NAM is standing up for manufacturers everywhere – from the halls of power where we advance important legislation, to the courts where we fight to defend our rights.

COSMA Impact Award Honors Minnesota Chamber of Commerce

Colorado Springs, Colorado –The National Association of Manufacturers announced that the Minnesota Chamber of Commerce was recognized by the Conference of State Manufacturers Associations with the first-ever COSMA Impact Award at the conference’s annual meeting this week. COSMA’s members serve as official state partners of the National Association of Manufacturers, focusing on manufacturing priorities at …

ICYMI: Jay Timmons Talks Manufacturing Tax Wins, AI’s Impact on Industry on “Mornings with Maria”

Washington, D.C. – National Association of Manufacturers President and CEO Jay Timmons

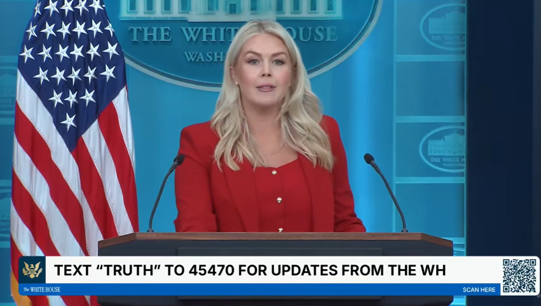

ICYMI: Karoline Leavitt Talks Manufacturing Success Stories, Cites NAM During White House Press Briefing

Washington, D.C. – White House Press Secretary Karoline Leavitt celebrated the pro-growth impacts of the Working Families Tax Cuts today in her press briefing. She cited the National Association of Manufacturers’ “

Manufacturers Warn Food Labeling Bill Would Raise Costs, Cause Uncertainty

Washington, D.C. – Following the approval of S. 5026 by the Senate Health, Education, Labor and Pensions Committee, National Association of Manufacturers Executive Vice President Erin Streeter issued the following statement: “Manufacturers support efforts to protect public health and give consumers clearer information, but legislation linking specific ingredients and food-processing methods to health risks without …

**Media Advisory** NAM to Host Capitol Hill Reception with Chairman Jason Smith to Celebrate Tax Wins Across America

Washington, D.C. – On Tuesday, July 21, the National Association of Manufacturers will host a Capitol Hill reception commemorating the one-year anniversary of H.R. 1. The event will feature remarks from House Ways and Means Committee Chairman Jason Smith (R-MO) and bring together manufacturers from across the country to highlight how the historic tax law …

NAM to Congress: Protect Innovation in America’s Defense Industrial Base

A proposed provision in the National Defense Authorization Act for Fiscal Year 2027 to remove the intellectual property rights of government contractors and expand the Pentagon’s access to the IP would undermine military readiness and disadvantage manufacturers, the NAM and more than two dozen allied groups recently told the House Committee on Armed Services. What’s …

ICYMI: To Bolster Workforce and Maintain Competitiveness, Manufacturers Boost Vaccines in New Report

Washington, D.C. – The National Association of Manufacturers today released a new report on workforce resilience and productivity, focused on the economic benefits of vaccines to prevent illness, lower healthcare costs and reduce absenteeism. As first reported by

ICYMI: NAM CEO Jay Timmons Talks USMCA, Energy and Jobs on Bloomberg’s Balance of Power

Washington, D.C.–This week, the National Association of Manufacturers President and CEO Jay Timmons joined Bloomberg’s Balance of Power to discuss the latest state of play on the United States–Mexico–Canada Agreement and what it means for manufacturers, the impact of the conflict in the Middle East on energy costs and the importance of American energy dominance …

NAM: Federal Court Ruling Is a Win for Manufacturers

Washington, D.C.–Following the U.S. District Court for the Eastern District of Pennsylvania’s decision denying plaintiff’s request to amend their complaint in Martinez v. Kraft Heinz Company, Inc., et al.—a ruling in favor of food and beverage manufacturers—National Association Manufacturers Chief Legal Officer & Corporate Secretary Linda Kelly released the following statement: “The Eastern District of …

NAM Joins Industry Leaders in Challenging Unconstitutional New Mexico Labeling Mandate

Washington, D.C.– Last night, the NAM joined industry leaders in filing a lawsuit to block New Mexico’s unconstitutional labeling mandate for products made with per- and polyfluoroalkyl substances, otherwise known as PFAS. “New Mexico’s PFAS product-labeling mandate compels manufacturers to spread the state’s unsupported message that any amount of any PFAS is dangerous, while unlawfully …