ICYMI: Iowa Manufacturer Expands, Credits Pro-Growth Tax Law

Vermeer Corporation Announces Plan to Build New Facility, Create 300+ Jobs

Washington, D.C. – Vermeer Corporation, an industrial and agricultural equipment producer based in Pella, Iowa, is crediting the pro-growth tax provisions of H.R. 1 with supporting the company’s plan to build an all-new 300,000-square-foot facility in the Des Moines metro that will create more than 300 jobs.

Vermeer said in a company statement, “We’re grateful for the state of Iowa, the pro-business environment, the skilled workforce here and economic policies, like Working Families Tax Cuts, that have helped support Vermeer’s long-term growth.”

Last August, National Association of Manufacturers Executive Vice President Erin Streeter joined Rep. Mariannette Miller-Meeks (R-IA) for a Made in America Manufacturing Tour across Iowa’s 1st District, where they visited Vermeer’s facility in Pella. During the tour, Vermeer President and CEO and NAM Executive Committee member Jason Andringa said H.R. 1 “sets up manufacturers for a generation of continued growth and advancement.”

Streeter praised Rep. Miller-Meeks’ leadership during the tour.

“H.R.1 is a landmark win for manufacturing—delivering pro-growth policies that will strengthen our industry for years to come. Without bold leadership from lawmakers like Rep. Miller-Meeks, manufacturers could have been crippled by the largest tax hike in history—jeopardizing the progress we made after the 2017 Tax Cuts and Jobs Act. Iowa’s 1st Congressional District is the first in the state for manufacturing. We want to thank her for protecting 13,000 jobs and $1.2 billion in wages at more than 800 manufacturing companies in her district alone.”

Background

KEY FACTS: If Congress had failed to preserve tax reform in 2025, the U.S. would have risked:

- 5.9 million lost jobs;

- A $540 billion reduction in employee compensation; and

- A $1.1 trillion shortfall in U.S. GDP.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

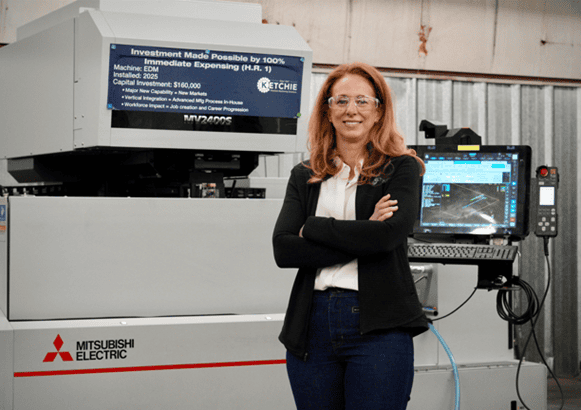

ICYMI: “Ketchie CEO Credits Trump’s ‘Beautiful Bill’ with Helping Her Machine Shop Prosper”

Washington, D.C. – As part of the 2026 National Association of Manufacturers State of Manufacturing Tour, Ketchie President and Owner Courtney Silver hosted the NAM for a discussion on how tax certainty due to the NAM-backed H.R. 1 has empowered manufacturers like her to reinvest in their workforce and facilities.

The tour stop was covered by Business North Carolina. Excerpts of the report can be found below. Bolding has been added.

—-

Ketchie CEO credits Trump’s ‘beautiful bill’ with helping her machine shop prosper

Business North Carolina

Kevin Ellis

Feb. 23, 2026

https://businessnc.com/ketchie-ceo-credits-trumps-beautiful-bill-with-helping-her-machine-shop-prosper/

Miguel Carrillo describes himself as a “machine nerd,” and he had an engaged audience on Monday watching him operate a $700,000 device brought in last year to Concord-based Ketchie, the machine shop where he works.

Ketchie may only have 20 employees, but it was a stop on the State of Manufacturing Tour that National Association of Manufacturers President Jay Timmons began last week in Cleveland and will continue across the country after visiting three Charlotte-area sites on Monday. Tagging along with Timmons at Ketchie was Acting Deputy Secretary of the U.S. Treasury Derek Theurer, U.S. Rep. Tim Moore of Cleveland County and NC Chamber President Gary Salamido.

Ketchie CEO Courtney Silver was a supporter of the “One Big Beautiful Bill,” the legislation signed into law last year by President Donald Trump. She testified at congressional hearings before its passage about how it would help small businesses. Timmons said he had heard so much about Ketchie’s new machines, he wanted to see them in action.

The tax bill that eliminates income tax on overtime and tips for some workers also allows businesses to reduce their tax bills on investments immediately, rather than spreading the reduction out over several years, says Silver.

“When you can expense an investment in the year it was purchased, it provides cash flow to companies and continues to allow them to make new investments,” says Silver.

Ketchie purchased three machines last year that combined cost more than $1.1 million, plus made about $400,000 in other investments, including AI software that has cut some hour-long processes down to five minutes.

“I would have never made those investments without immediate expensing,” Silver says. She says she’s also looking to add five workers to her shop.

“This is a perfect example of what you can do to help build America and American manufacturing with the right policies in place,” says Timmons.

Theurer said it was nice to see advanced manufacturing take place in a North Carolina factory rather than spending his day on policy in the nation’s capital.

“This type of investment is what we intended to see when we made our big tax policy and worked for smarter regulation,” said Theurer.

…

Ketchie supplies metal parts to railroad, aerospace and heavy industry manufacturers, such as Charlotte steelmaker Nucor, Davidson-based HVAC company Trane and Norfolk Southern. The company was started in 1947 by Edgar Ketchie, the grandfather of Silver’s late husband.

On Monday, Carrillo was machining a steel part needed by an industrial recycling company. The Dual Spindle 5-Axis Machining Center that Ketchie bought last year doesn’t require Carrillo to reset the machine for the other side of the metal part, which is about half the size of a deck of cards, but grooved. It means quicker production and fewer human errors, he says.

“It allows me to step out and allows the machine to do the heavy lifting,” says Carillo. The advanced manufacturing aspect attracted the 2024 graduate of A.L. Brown High School to work at Ketchie after starting in a job shadowing program while a high school junior. “It’s nice when a machine can do one thing, but it’s really nice when a machine can do a lot of things.”

…

—-

Background

Learn more about Silver’s testimony before Congress in 2025 on the importance of preserving the pro-manufacturing policies of the Tax Cuts and Jobs Act here.

KEY FACTS: If Congress had failed to preserve tax reform in 2025, the U.S. would have risked:

- 5.9 million lost jobs;

- A $540 billion reduction in employee compensation; and

- A $1.1 trillion shortfall in U.S. GDP.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

NAM Tour Highlights How Tax Reform Fuels Growth in North Carolina

2026 NAM State of Manufacturing Tour Stops in Charlotte and Concord, North Carolina

CHARLOTTE – The National Association of Manufacturers—official partner of America250—in partnership with the North Carolina Chamber, continued its 2026 NAM State of Manufacturing Tour today in Charlotte and Concord, North Carolina, under the theme “Competing for the Future.”

The tour stop highlighted how the NAM-backed H.R. 1 is creating a more competitive tax environment—and why sustaining that certainty, along with regulatory rebalancing, modern infrastructure and reliable energy, is critical to driving continued investment and job creation across the sector. Today’s visits included Ketchie Inc., Siemens Energy and Electrolux.

“Here in North Carolina, we’re seeing exactly what tax certainty makes possible,” said NAM President and CEO Jay Timmons. “Thanks to President Trump and leaders in Congress, the pro-growth provisions in H.R. 1 were made permanent and strengthened, delivering a win for manufacturers of all sizes. To make the United States the best place in the world to do business and so manufacturers across North Carolina can keep investing, hiring and competing, we must build on that tax foundation we secured. That means enacting comprehensive, commonsense permitting reform to unleash American energy dominance, driving the funding we need for strong, modern infrastructure, modernizing regulations, investing in our manufacturing workforce and implementing smart AI policy—all through a comprehensive manufacturing strategy.”

Ketchie President and Owner Courtney Silver hosted the first stop of the day with a tour and panel discussion on how tax certainty due to the NAM-backed H.R. 1 has empowered manufacturers like her to reinvest in their workforce and facilities. Silver emphasized that pro-growth tax policies, such as permanent full expensing, have enabled business owners to remain agile and competitive. With that tax certainty in place, Ketchie has invested in new critical machinery—expanding capacity, increasing efficiency and positioning the company to hire, grow and compete for the long term.

The tour then moved to Siemens Energy, which recently announced a $421 million expansion in North Carolina to grow its large power transformer manufacturing and continue gas turbine production in Charlotte—an investment expected to create 500 new jobs statewide.

The day concluded at the North American headquarters of Electrolux, the global home appliance manufacturer, employing hundreds in the Charlotte region.

Throughout the day, business leaders highlighted the impact of North Carolina’s nearly 500,000 manufacturing workers who make up more than 11% of the workforce and power the largest manufacturing sector in the Southeast.

Timmons was joined by North Carolina Chamber President and CEO Gary Salamido and other NAM leaders throughout the day. Deputy Secretary of the Treasury Derek Theurer and Rep. Tim Moore (R-NC) participated in the visit to Ketchie.

“Thanks to America First policies, domestic manufacturing is back, and we’re seeing serious investments right here in North Carolina,” said Rep. Moore. “It was great to join the National Association of Manufacturers at Ketchie alongside Deputy Secretary of the Treasury Derek Theurer to see firsthand how tax certainty and pro-growth policies are giving companies the confidence to expand and compete with anyone in the world.”

“North Carolina’s manufacturers are a major driver of our state’s economy, contributing a higher-than-average 15% of our gross state product,” said Salamido. “With a manufacturing tradition like ours, we are proud to partner with the NAM to show the nation that our state is the premier destination for manufacturing, so long as pro-business policies allow for it.”

From Charlotte, the 2026 NAM State of Manufacturing Tour will go on to Milwaukee, Wisconsin; Dallas and Houston, Texas; and Phoenix, Arizona. The tour made stops in New York City, Cleveland and Pennsylvania prior to today’s events in Charlotte. Throughout the tour, the NAM will continue meeting with policymakers, manufacturers of all sizes, students and business leaders, advocating for the people and policies that will ensure the United States is the best place in the world to do business. To learn more about the tour and the NAM’s mission, visit https://nam.org/stateofmfg/.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Innovation Takes Center Stage as Manufacturers Launch NAM State of Manufacturing Tour from the Rock & Roll Hall of Fame

CLEVELAND – The National Association of Manufacturers today kicked off its annual NAM State of Manufacturing Tour, a cross-country sprint spotlighting the vital role that manufacturing plays in supporting the nation’s economy. On the first leg of the tour, NAM President and CEO Jay Timmons and other leaders underscored the state’s industrial momentum while calling on our nation’s leaders to pursue a comprehensive manufacturing strategy—building on permanent, pro-growth tax reform manufacturers secured last summer.

“Innovation Built America. Manufacturing Wins the Future” is the theme of this year’s tour, and framed a series of events in Cleveland, bringing together industry leaders, students and policymakers to spotlight Ohio’s nearly 700,000 manufacturing employees—about 12% of the state’s workforce.

“There’s no better place to start a road tour than the Rock & Roll Hall of Fame,” said Timmons, an Ohio native, at the iconic Rock & Roll Hall of Fame, where he delivered his 13th NAM State of Manufacturing Address. “Like rock ‘n’ roll, manufacturing is everywhere. We are hitting the road to showcase the world-leading innovation happening across the country and how we make the next 250 years even greater. Manufacturers are ready to invest—and we need certainty, like the tax bill delivered last year. Permanent tax reform gave manufacturers the rocket fuel. Now we need clear skies. That’s energy dominance, permitting reform, trade certainty, investing in the manufacturing workforce and smart AI policy.

Timmons was joined by Rockwell Automation Chairman and CEO and NAM Board Chair Blake Moret, Cleveland Mayor Justin Bibb, EQT Corporation President and CEO and NAM board member Toby Z. Rice, The Ohio Manufacturers’ Association President Ryan Augsburger and NAM Executive Vice President Erin Streeter. Following the address, Timmons and Moret hosted a student reception at the Hall of Fame, where they engaged with the next generation of creators. The tour then moved to the Rock Hall’s “Jam Garage” for a unique filming opportunity showcasing the intersection of culture and industry. The setting provided a compelling backdrop for discussions about the connection between manufacturing and rock ‘n’ roll—two distinctly American traditions that involve bold ideas, creative risk-taking embracing technological change and the ability to shape global culture.

“The innovation we’ve seen Ohio manufacturers embrace over time is exactly why this tour is so vital,” said Moret. “At Rockwell, we see every day how automation and AI are redefining what’s possible on the factory floor. By visiting places like Cleveland State University and seeing the talent being cultivated here, it’s clear that Ohio manufacturers are moving at the speed of business. Now, we must ensure the federal government keeps up with that pace.”

The afternoon featured an in-depth tour and lunch at EY-Nottingham Spirk Innovation Hub followed by a final stop at Cleveland State University to discuss the critical intersection of higher education and industrial workforce development.

“Ohio’s manufacturers are the backbone of our state’s economy, and having the national tour stop here in Cleveland underscores the importance of our mission,” said Augsburger. “We are proud to stand with the NAM to advocate for the policies that will keep our nearly 700,000 manufacturing workers at the forefront of global competition.”

From Cleveland, the 2026 NAM State of Manufacturing Tour will go on to Philadelphia, Pennsylvania; Charlotte, North Carolina; Milwaukee, Wisconsin; Dallas and Houston, Texas; and Phoenix, Arizona. Throughout the tour, the NAM will continue meeting with policymakers, manufacturers of all sizes, students and business leaders, advocating for the people and policies that will ensure the United States is the best place in the world to do business. To learn more about the tour and the NAM’s mission, visit www.nam.org.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

Treasury Clears Path for Greater Manufacturing Investment with Tax Proposal on CAMT

Washington, D.C. – Following the release of a new proposal from the Department of the Treasury reforming key aspects of the Corporate Alternative Minimum Tax guidance and addressing the interaction between the immediate expensing of R&D costs and the CAMT, National Association of Manufacturers Managing Vice President of Policy Charles Crain released the following statement:

“Congress and the Trump administration passed a once-in-a-generation tax law last summer, and now Treasury is building on that win.

“The Corporate Alternative Minimum Tax has threatened manufacturers’ ability to raise wages, hire workers and invest in their communities since it was enacted in 2022. With today’s proposal, Treasury has taken a step toward fixing this fundamentally unworkable regime.

“In particular, the proposed changes to protect H.R. 1’s restoration of immediate expensing for R&D costs will ensure manufacturers are not penalized for their commitment to making investments that drive innovation. Manufacturers conduct 52% of private-sector research—investments that will continue to drive the industry and the economy given that 80% of manufacturers say AI innovation will be essential to grow or maintain their business by 2030.

“The Trump administration is meeting the moment by taking urgent action to supercharge private-sector R&D. Manufacturers called for this critical change, and we thank Treasury for taking this important step to support manufacturing innovation and ensure the continued success of H.R. 1 for our industry.”

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.95 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

A Century-Old Manufacturer and the Town It Supports

Draper, Inc. is an unusual manufacturer: a company with 700 employees located in a town—Spiceland, Indiana—with only 900 residents. Draper President Chris Broome said the town would “look a lot different” without Draper, and the company has “grown with the community”—hiring many residents of Spiceland, working closely with the school system, supporting the town library and community center, helping with cleanup efforts and much more.

Since 1902: Draper was founded near the start of the 20th century. A family-owned firm now helmed by the fifth generation—and looking ahead to the sixth—Draper began by manufacturing window shades. Since its founding, it has expanded into many other product lines, including projection screens and gym equipment.

- Broome is the great-great-grandson of founder Luther O. Draper, and he says with pride that his son now works as a regional salesperson—and is expected to step into the leadership role someday.

Staying in Spiceland: The company’s relationship to Spiceland, meanwhile, is one of deep commitment and respect. Many of the company’s employees live in the town itself, though some live in neighboring locations.

- The company’s longstanding residence in Spiceland has allowed it to create a singular workforce—where people stay for 20, 30, even 40 years, said Broome.

- Just like the company’s founding family, these employees often pass down their commitment to Draper. There are “families of two to three generations” who work at the company—which is “unique and really interesting,” said Broome.

- One factory department head has been at Draper for 53 years, having started right after high school. Both his parents worked at Draper, too, Broome added.

Recruitment: The company encourages its workers to “grow with the company” and recruits heavily from local high schools. Not only do local highschoolers take internships at the company, but whole classes come to Draper for tours.

- Draper works closely with the school system to place interns in exactly the right department, with the strong support of Indiana’s state educational department, said Broome.

- The students do “real work” for the company, he stressed, adding that one of the program’s key benefits is the way it teaches kids basic skills applicable to any working environment—like showing up on time and not getting distracted by their phones.

- “We’re really trying to teach them the basics for having a career in the future, to expose them to possibilities,” said Broome.

Policy talk: Broome credits tax reform with enabling the expansion of his remarkable company.

- First, the 2017 Tax Cuts and Jobs Act’s provisions—made permanent last year in the One Big Beautiful Bill Act—helped Draper build its new 100,000-square-foot facility, said Broome. Draper also “invested in equipment and automation, including a new automated paint line,” as well as solar panels for the new facility’s roof that now provide about 40% of its electricity, thanks to the bill’s provision for immediate expensing for equipment purchases.

- Second, tax reform’s estate tax measure—also made permanent last year—has helped the company plan for its future. Broome now has “much more certainty about preserving the company for the future and the ability to pass it down from generation to generation,” he said.

A new century: What is Draper working on in its second century? Automation and artificial intelligence are “important initiatives,” said Broome.

- Draper has created a cross-functional employee group to explore how AI can be built into many daily functions, an initiative that has begun to pay off already. Meanwhile, automating some manual parts of production, like pushcarts and spray guns, has helped Draper streamline and regularize operations, while freeing workers to do higher-level tasks.

- “We know that to be competitive in the worldwide economy, we will have to focus on doing more,” Broome concluded.

ICYMI: NAM’s Charles Crain Testifies Before House Small Business Committee

Washington, D.C. – Today, National Association of Manufacturers Managing Vice President of Policy Charles Crain testified before the House Small Business Committee at its hearing, “Made in the USA: How Main Street Is Revitalizing Domestic Manufacturing.”

In his testimony, Crain thanked the Small Business Committee for its leadership on the recent tax reform package, which made pro-growth, pro-manufacturing tax policy a permanent part of the tax code, giving small and medium-sized manufacturers much-needed certainty. However, by addressing other ongoing challenges, Congress can strengthen and protect the success of H.R. 1.

In his opening remarks, Crain outlined the opportunities:

“Congress and the administration can pursue what we’ve called a ‘comprehensive manufacturing strategy.’

- That means rebalancing unworkable regulations and reforming America’s broken permitting process;

- It means investing in our nation’s infrastructure and supporting American energy dominance;

- It means providing trade certainty that empowers manufacturers to make things in America;

- And it means investing in the manufacturing workforce of the future.

“We need all of these policies to build on the success of tax reform, to unlock small manufacturing growth and to drive a true manufacturing renaissance.”

He closed his remarks by encouraging the committee to build on this year’s success:

“This is the road to a manufacturing renaissance. It runs through a comprehensive manufacturing strategy—ensuring that all parts of the federal government are rowing in the same direction: toward an empowered, emboldened, exceptional manufacturing industry.

“Backed by the right policy choices, small manufacturers will deliver—for our communities, for our country and for our preeminence on the world stage.

“Because when manufacturing wins, America wins.”

Read Crain’s full written testimony here.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

NAM Taps Industry Veteran Jake Kuhns as Vice President of Domestic Policy

Policy Expert to Drive Food and Beverage, Tax, Health Care, Technology and Immigration Issues for Manufacturers

Washington, D.C. — The National Association of Manufacturers today announced the addition of Jake Kuhns as a vice president of domestic policy at the association. Kuhns, a public policy professional with more than two decades of experience in federal government relations—including shaping policy for Cargill’s food business—will lead the NAM’s work on food and beverage policy, tax, corporate finance, health care, artificial intelligence and technology and immigration.

“Jake brings a wealth of relevant knowledge and experience from his more than 20 years working at the intersection of policy, politics and business, including his work on food and beverage issues that are vital to manufacturers nationwide,” said NAM President and CEO Jay Timmons. “This is a pivotal time for manufacturers as our industry navigates a shifting policy landscape. The landmark tax bill signed into law on July 4 will stimulate investment across manufacturing, but these investments will require a comprehensive manufacturing strategy that builds on our tax win in order to achieve the law’s full pro-growth potential.”

For more than 13 years, Kuhns served as director of federal government relations for Cargill, one of the world’s largest manufacturers of food, beverage and agricultural products. In that role, he led advocacy efforts on food and beverage issues, antitrust and competition, labor and immigration, transportation and tax. He regularly advised Cargill’s senior leadership on the policy and political landscape, managed the company’s political action committee and represented the corporation before Congress, the administration and key federal agencies. His previous experience includes serving as a senior legislative aide to Rep. Tim Holden (D-PA), as well as both association and campaign work.

Timmons added, “Jake is a veteran of our sector and understands the needs of manufacturers. Under his leadership, the NAM will continue to work with Congress and the administration to protect and implement H.R. 1, seize the opportunities presented by artificial intelligence, address the rising costs of health care, support capital formation and good corporate governance, modernize and rebalance federal regulations and ensure that innovators across manufacturing—including biopharmaceutical manufacturers and companies throughout the food and beverage supply chain—can continue to innovate, grow and thrive here in America.

“As manufacturers look to build on recent policy wins and usher in generational change for the sector, we are excited to add Jake to our best-in-class policy team.”

With the recent passage of H.R. 1, Kuhns’ immediate attention will turn to the implementation of the tax package and advancing a comprehensive domestic manufacturing agenda that drives growth, competitiveness and innovation.

Kuhns joins the NAM’s powerhouse external affairs team under the leadership of Executive Vice President Erin Streeter, who oversees the association’s advocacy, policy, government relations and communications efforts. He will report to Managing Vice President Charles Crain, head of the NAM’s policy shop propelling the manufacturing agenda forward, and will work alongside Vice President of International Policy Andrea Durkin, Vice President of Domestic Policy Chris Phalen and Chief Economist Victoria Bloom.

Kuhns is the latest in a wave of 2025 hires across the NAM’s external affairs division, including Senior Director of Tax Policy Connor Rabb, Senior Director of Corporate Finance Policy Ted Allen, Director of Government Relations Sydney Fincher, Director of Health Care Policy Jess Wysocky, Director of Chemicals, Materials and Sustainability Policy Reagan Giesenschlag, Director of International Policy Kevin Doyle, Vice President of Communications and Public Affairs Alexa Lopez, and Director of Strategic Communications Christine Ravold. In addition to adding new talent to the NAM’s team, veteran NAM staff members Jennifer Littlepage and Joseph Murphy have been elevated to vice president of human resources and director of strategic communications, respectively.

-NAM-

The National Association of Manufacturers is the largest manufacturing association in the United States, representing small and large manufacturers in every industrial sector and in all 50 states. Manufacturing employs nearly 13 million men and women, contributes $2.90 trillion to the U.S. economy annually and accounts for 53% of private-sector research and development. The NAM is the powerful voice of the manufacturing community and the leading advocate for a policy agenda that helps manufacturers compete in the global economy and create jobs across the United States. For more information about the NAM or to follow us on Twitter and Facebook, please visit www.nam.org.

ICYMI: Iowa Manufacturers Thank Rep. Mariannette Miller-Meeks for Backing Pro-Growth H.R. 1 on Shop Floor Tour

Washington, D.C.–Iowa manufacturers today rolled out the welcome mat for Rep. Mariannette Miller-Meeks (R-IA-01), thanking her for her support of H.R. 1 during a three-stop shop floor tour as part of the congresswoman’s “Made in America Manufacturing Tour” across Iowa’s 1st Congressional District.

National Association of Manufacturers Executive Vice President Erin Streeter and Iowa Association of Business and Industry President Nicole Crain joined the congresswoman in visiting Cemen Tech, Vermeer and SSAB. Each stop underscored how the manufacturing law is already fueling growth, strengthening competitiveness and creating opportunity in Iowa communities.

Photo Credit: David Bohrer/National Association of Manufacturers

Crain said, “We appreciate Rep. Miller-Meeks’s longtime support of Iowa manufacturers. From her service in the Iowa Senate to her work in Congress, she has been a consistent advocate for pro-growth tax policies. ABI members thrive on certainty, and this legislation gives Iowa businesses the stability they need to reinvest in their people and their operations.”

In Indianola, Rep. Miller-Meeks toured employee-owned Cemen Tech, the world’s largest manufacturer of volumetric concrete mixing systems.

Cemen Tech Director of Supply Chain Brant Pfantz thanked Rep. Miller-Meeks for her support. “We are so grateful to Rep. Miller-Meeks for voting for pro-growth tax reform. It’s not just about giving manufacturers like us certainty but giving our contractors—builders and developers—the certainty to plan for their next projects so we can all build and scale together.”

Photo Credit: David Bohrer/National Association of Manufacturers

The second stop, at industrial and agricultural equipment producer Vermeer Corporation, demonstrated how provisions like renewing the research and development deduction in the tax package will help manufacturers maintain their competitiveness.

Vermeer President and CEO Jason Andringa said, “The Big Beautiful Bill will allow us to continue to deduct expenses related to research and development. This is critical if manufacturers are going to continue to push the edge and innovate. This bill sets up manufacturers for a generation of continued growth and advancement.”

Global steel manufacturer SSAB hosted the final stop on the tour. SSAB Americas President Chuck Schmitt reiterated how important H.R. 1 is to the U.S. manufacturing economy. “The One Big Beautiful Bill Act will act as a growth catalyst for manufacturing in America. By driving investment, strengthening supply chains and ensuring our workforce has the tools and training to succeed, this law will help SSAB meet growing demand with the most sustainably produced American-made steel. We thank Congresswoman Miller-Meeks for her continued leadership on policies that support jobs, improve competitiveness and strengthen our nation’s economy.”

-NAM-

Manufacturers Host Lawmakers, Celebrate Tax Reform Victory

Manufacturers in Pennsylvania and New Jersey welcomed Republican representatives to their facilities this week, thanking them for delivering a landmark victory for manufacturers: the passage of H.R. 1.

- House Republican Conference Chairwoman Lisa McClain (R-MI) and local Reps. Tom Kean (R-NJ-7), Rob Bresnahan (R-PA-8) and Ryan Mackenzie (R-PA-7) participated in the factory tours as part of Chairwoman McClain’s One Big Beautiful Tour.

NAM in action: NAM Executive Vice President Erin Streeter accompanied lawmakers, highlighting how the Manufacturing Law is already having positive impacts on local manufacturing.

- “Manufacturing is the backbone of the American economy—and with the leadership of Chairwoman McClain, Reps. Kean, Bresnahan, Mackenzie and their colleagues in Congress—that foundation is stronger than ever,” Streeter said following the visits.

- “By championing the Manufacturing Law, Congress has protected nearly 6 million jobs and more than $500 billion in wages for hardworking Americans. We thank them for their leadership.”

New Jersey: Chairwoman McClain and Rep. Kean toured Bihler of America , a manufacturer of precision automation systems in Phillipsburg, New Jersey. The company specializes in complex metal stamping, forming and assembly solutions, serving industries such as automotive, medical and consumer products.

- “Manufacturers thrive when we have the certainty we need to plan major investments in our facilities and our people. That’s exactly what this tax package delivers,” said Bihler CEO Maxine Nordmeyer.

- “We thank our partners in Congress and the administration—and we look forward to working with them on a full comprehensive manufacturing strategy. Through energy, trade and workforce policies that drive our competitiveness, deliver certainty and empower manufacturers, we will build on the success of the One Big Beautiful Bill.”

Pennsylvania: Rep. Bresnahan joined Chairwoman McClain for a tour of i2M , a manufacturer of flexible polymers in Mountain Top, Pennsylvania. The company produces custom polymer films and sheets used in a variety of applications, including agriculture, construction, packaging and geomembranes.

- “Manufacturers are innovators. By restoring immediate R&D expensing for manufacturers across America [a key provision of the OBBBA], Congress has empowered manufacturers like i2M to innovate and create,” said i2M Founder Chris Hackett.

- “That’s how we keep our competitive edge—not just as a company, but as a country.”

Pennsylvania, round 2: At another stop in the Keystone State, Rep. Mackenzie joined the tour at U.S. Metal Powders in Palmerton. The visit highlighted the company’s recent expansion, including a new state-of-the-art production line that will create new jobs and boost aluminum powder output for global markets.

- “Thanks to this transformative tax legislation, U.S. Metal Powders has already broken ground on adding another production line—which will soon double the company’s workforce. This is pro-growth tax policy in action,” Pennsylvania Manufacturers’ Association President and CEO David N. Taylor said in response to the visit.

NAM in the news: The White House’s rapid response account on X highlighted Rep. Bresnahan’s visit to Pennsylvania and appearance on the area’s local Fox affiliate.

- Fox Business Network’s Maria Bartiromo cited the NAM’s partnership on the tour in an interview with Chairwoman McClain.

- The House GOP X account shared a video of Streeter talking about the facility visits.

- Chairwoman McClain posted about her visits to Bihler of America, i2M and U.S. Metal Powders on X. Chairwoman McClain, along with Reps. Bresnahan and Kean, also amplified the NAM’s own social posts.

- WVIA covered the visit to i2M.